When it comes to saving for retirement, there are various tax-advantaged accounts to choose from. Each type of account offers different tax treatments, which can affect how much you pay in taxes both now and in the future. Here’s a breakdown of the three main types of retirement accounts and their tax treatments: Traditional IRA or 401(k), Roth IRA or 401(k), and taxable accounts.

Traditional Accounts

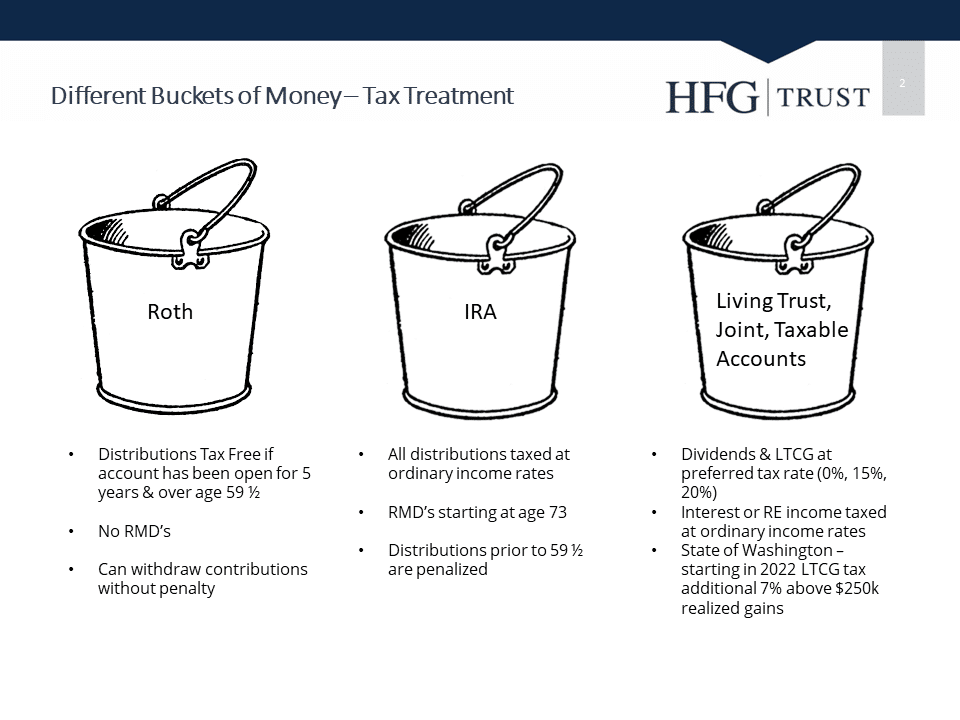

A traditional IRA (Individual Retirement Account) or 401(k) is a tax-deferred retirement account. This means that contributions you make to the account are made with pre-tax dollars, reducing your taxable income in the year you make the contribution. For example, if you earn $50,000 a year and contribute $5,000 to a traditional IRA, your taxable income for the year will be reduced to $45,000. You won’t have to pay taxes on that $5,000 until you withdraw it from the account in retirement. When you do withdraw the money, it will be taxed as ordinary income.

In addition to the tax-deferred contributions, traditional IRA and 401(k) accounts have required minimum distributions (RMDs) once you reach age 73. These are mandatory withdrawals that you must take from your account each year. The amount of the RMD is calculated based on your age and the value of your account. Failure to take the required minimum distribution can result in a penalty of up to 25% of the amount that should have been withdrawn.

Roth Accounts

A Roth IRA or 401(k) is another type of retirement account. Contributions to a Roth account are made with after-tax dollars, meaning you don’t get a tax deduction in the year you make the contribution. However, the money grows tax-free while it’s in the account, and you won’t have to pay taxes on any of the withdrawals you make in retirement. This includes both your contributions and the investment earnings.

One important thing to note is that Roth IRA and 401(k) accounts are not subject to required minimum distributions. This means that you can let the money in the account continue to grow tax-free for as long as you want, without having to withdraw a certain amount each year.

Also note that for both traditional and Roth retirement accounts, you will be penalized for withdrawals that occur prior to age 59 ½. These accounts are intended to be used for retirement and have been incentivized by the tax benefits they offer when making contributions. Taking funds from retirement accounts early can create both penalties and taxable events. There are exceptions to these penalties, but you should review your situation with a financial advisor to see if you qualify.

Taxable Accounts

A taxable account is an investment account that is not specifically designated as a retirement account, and they do not share any of the tax-advantaged benefits of qualified retirement accounts. However, they do provide flexibility in a financial plan that can be very helpful.

- Contributions to a taxable account are made with after-tax dollars, meaning you won’t get a tax deduction in the year you make the contribution.

- Any income created by the portfolio, such as interest and dividends, will be taxed in the year earned. Some of which will be subject to preferential capital gains tax rates.

- Any appreciation of assets will be taxed as capital gains in the year the assets are sold.

Due to the taxable nature of these accounts, asset selection is very important. They are more flexible in that there are no contribution age restrictions and distributions can be taken at any time without penalty. They are less flexible in that a rebalance or selling out of an investment and buying into another causes a taxable event. It is important to understand your objectives with your taxable account and build a tax efficient strategy around those objectives.

There are several types of tax treatments for retirement accounts, each with its own benefits and drawbacks. Traditional accounts offer tax-deferred contributions but have required minimum distributions. Roth accounts require contributions to be taxed but offer tax-free growth and no required minimum distributions. Taxable accounts offer more flexibility overall but are more constrained by tax law.

It’s important to understand your options and choose the best retirement account for your specific financial situation. Contact an HFG Trust advisor today to help determine which accounts will be best to help you reach your goals.