In 1970 more than 45% of all private sector employees in the United States were covered by some kind of pension plan. As of 2022, that number is around 4%. What does this dramatic difference mean for the present-day worker? Well, the truth is, the next generation of retirees will rely on their own savings and a 401k to supplement their income in retirement.

Whilst employers have been moving away from the traditional pension plan, the 401k plan has massively increased in popularity. In fact, 67% of private sector companies offer a 401k or similar employer sponsored retirement savings plan to their employees today.

These retirement savings plans are a great benefit, but for employees to capitalize, they often must opt-in to participate in the plan. So, what exactly are the benefits of participating in your employer’s 401k plan?

Employer Matching Contributions

Perhaps the biggest benefit of participating in a 401k plan is that it is the only account where you can receive a guaranteed 100% return. That return is in the form of an Employer Matching Contribution.

Most 401(k) plans have an employer match that incentivizes employees to contribute to the 401k. A lot of the time the match will be something like: For every 4% of your income that you contribute, your employer will contribute 4%. Or, on the first 3% of your income that you contribute, your employer will match 100%, and on the next 2% of your income that you contribute, your employer will match 50%. The second scenario calculation computes too, if you contribute 5% you will receive a 4% match.

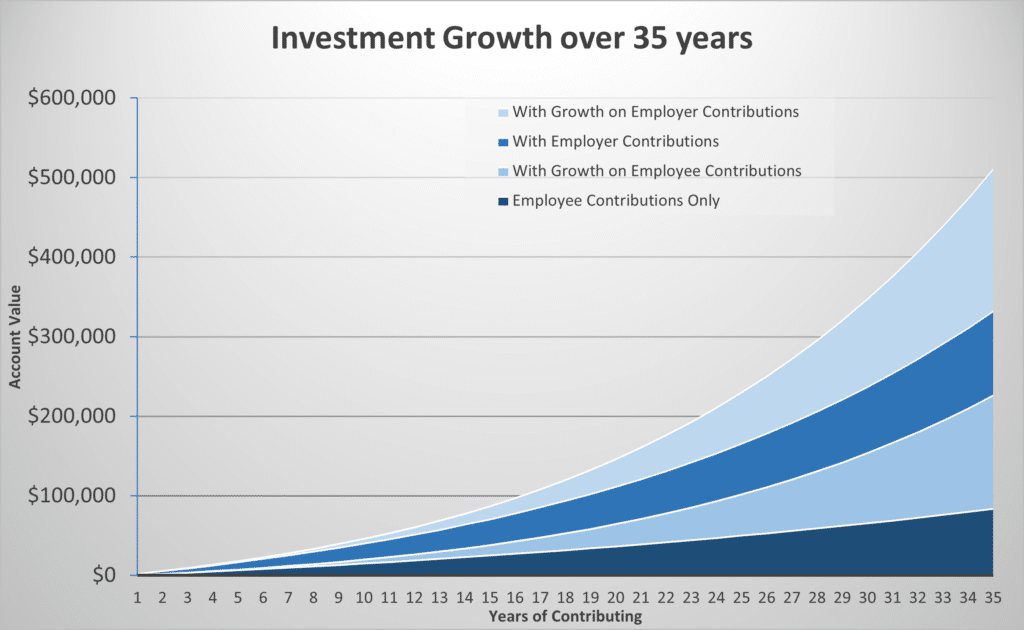

As you can see, employer matching is essentially free money. Because of this, it is important for you to maximize your employer match, or you will be leaving money on the table. The chart below shows the drastic difference that employer matching contributions can make during a 35-year career.

Tax Advantages of a 401k

When the IRS wrote section 401(k) of the tax code, they allowed for some nice tax breaks to those who want to save for retirement. Today, most 401k plans offer two options: Roth or Pre-tax. These are how the dollars contributed will be treated from a tax perspective.

Roth

When you contribute to a Roth 401k, your deferrals are on an after-tax basis so you don’t get any tax breaks today, but any growth in the account is tax-free and you can withdrawal funds tax-free after you turn age 59 ½.

Pre-Tax (Traditional)

When you contribute to a Pre-Tax 401k your deferrals are on a pre-tax basis. This option allows you to subtract your deferrals from your taxable income. For example, if you earn $60,000 in taxable income and you contribute $5,000 annually to your Pre-Tax 401(k), then your taxable income for the year will decrease to $55,000.

Generally speaking, if you feel that you are going to be in a higher tax-bracket in retirement or you have a long time until you plan to retire, Roth contributions are the way to go because you are better off paying lower taxes today than higher taxes in the future. Plus, if you are young and invested more aggressively in a stock-heavy portfolio, you will be able to take advantage of 30+ years of tax-free returns.

On the contrary, if you are a high-income earner and expect that you will spend less money in retirement, you are probably better off contributing to the pre-tax retirement account to take advantage of the tax break today while you are in a higher tax bracket.

Lastly, most 401k plans give you an option to make both Pre-Tax and Roth contributions at the same time. So, depending on your situation, that could make sense as well. As always, everyone’s situation is different, and you are best off speaking with a Certified Financial Planner™ who can help you make the best decision for you.

Long Term Retirement Savings

The third and final reason you should be investing in your 401k is perhaps the most obvious: Long-Term Retirement Savings. As mentioned before, pensions are a thing of the past for most people, and Social Security is only designed to replace about 40% of your income. This is not enough for most people to live on in retirement. To supplement the 60% of income Social Security does not cover, it is necessary to be investing in your own personal retirement account(s) to help bridge the gap.

Part of what is so great about 401k plans is that they are designed to be long-term savings accounts. Generally, you aren’t able to take distributions (except for loans and hardships) from your account while you are working for your employer, and you are penalized for taking cash distributions from the account prior to turning 59 ½. These guardrails are in place to ensure that you keep your money in the account, invested, and growing for your retirement goal.

A 401(k) is an integral part of your financial plan. For many, a 401k will make up the largest source of income through retirement.

If you have any questions about how you should be investing within your 401k, what kind of contributions you should be making, how much you need to be saving, or if you would like to discuss other financial planning options, contact an HFG Trust Financial Advisor.

Tyler Pearson

Wealth Planner