Think about the last time you had a year-end bonus. After you went out for a nice dinner and topped off your car’s gas tank, you probably sat down and thought about the best way to invest the money.

People come into a lump sum of cash more often than you might think. Be it a year-end bonus, an inheritance, or even a lucky lottery ticket, the same concern often arises – Should it all be invested at once?

When faced with this situation, you generally have three options:

- Deposit the money into a bank account

- Invest it as a lump sum

- Invest the funds using the Dollar-Cost Averaging method

Most people are aware of the dangers that come with leaving cash in the bank – earning a low interest rate allows for inflation to eat into the purchasing power, leaving you with less and less as time goes on.

This leaves us to decide between the other two options. Should we invest the lump sum today or implement a dollar-cost averaging strategy?

Before we get too far, let’s define what dollar-cost averaging is. We can explain dollar-cost averaging as the practice of investing a fixed dollar amount on a regular basis, regardless of the share price. For example, let’s say Tom inherits $100,000 in cash. The dollar-cost averaging approach might have him purchase $10,000 worth of stock every month for 10 months until he has invested $100,000.

The advantage of dollar-cost averaging is that Tom spreads his investment across different prices over the course of those ten months. If stock prices decline over those 10 months, he benefits by purchasing shares at progressively lower prices compared to investing the entire $100,000 all at once. However, if share prices rise, investing the full $100,000 upfront would have been advantageous.

Now that we understand the basics of dollar-cost averaging, let’s tackle the big question – which strategy is better for you?

At face value, the answer depends on how the stock market performs over the course of time that you would have implemented dollar-cost averaging. For instance, if you chose to invest a lump sum in January instead of dollar-cost averaging over the course of 12 months you would be better off if the stock market experienced gains for the year. You would be worse off if the stock market experienced losses. So, the answer is that it depends on how the market performed. But we can do better than that.

We know a couple things to be true as stock investors.

- Timing the market is difficult and often results in poor outcomes

- The stock market experiences gains more often than it experiences losses

If we know that an increase in stock prices results in an advantage for the lump sum investor and we know that a decrease in stock prices results in an advantage for those using dollar-cost averaging, we should make our decision based on our outlook on how stock prices will behave in the short term, right?

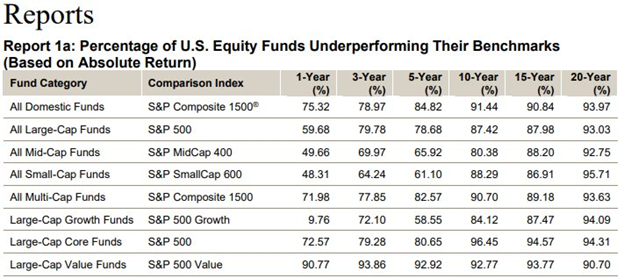

Nope. Below is a chart showing that even professional mutual fund managers, hedge fund managers, and financial analysts can’t predict the stock market with consistent accuracy.

If they can’t get it right more than 50% of the time, then the common investor definitely shouldn’t be trying to outsmart the market.

As we covered above, truth number one tells us we should not be betting on ourselves to predict where the market is going. Great! Well, that leaves us right where we started, should we dollar-cost average or should we just invest the lump sum and be done with it?

Truth number two should shed some light on the topic. If the stock market goes up more often than it goes down, then often, the investor is better off investing a lump sum than they are dollar-cost averaging.

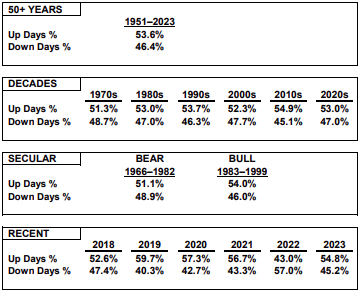

As you can see above, positive return days are more common than not in the stock investing world, though not by much. But as we look at months, we see that percentage grow to 57% of months being positive. By the time we reach annual returns we learn that 73% of years show positive returns in the S&P 500.

Why does this matter? Because as investors we can use this information to help us decide between lump sum investing and dollar-cost investing.

As we have already covered, if the market goes up, we gain an advantage by investing the lump sum all at once. If the market goes down, we gain an advantage through dollar-cost averaging. Knowing now that the stock market performs positively more often than negatively, we know that more often than not we are gaining an advantage by investing the lump sum.

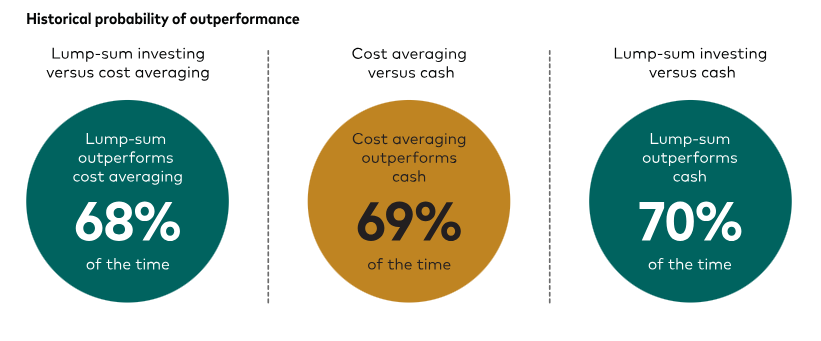

Furthermore, assuming a one-year investment horizon for dollar-cost averaging, a Vanguard study shows the historical probability of outperformance for the lump sum investor over dollar-cost averaging is 68%, statistically relevant enough to make the case for lump sum investing over dollar-cost averaging. Other findings of the paper showed that dollar-cost averaging out-performed cash 69% of the time and lump sum investing outperformed cash 70% of the time.

Statistically speaking, lump sum investing is advantageous comparatively to dollar-cost averaging, but the outperformance is not guaranteed. As discussed, investors don’t know what the market is going to do. Thus, there is more that needs to be considered than just what we think the market is going to do. Dollar-cost averaging is the safer and less volatile way of investing a large portion of cash. For this reason, there is a good argument that risk adverse investors should go the dollar-cost averaging route. Likewise, if you feel that stock prices are high, that could be reason to decide in favor of dollar-cost averaging. However, if you want to play the statistics and you have the capacity and tolerance for risk and volatility, then investing your lottery winnings all at once is the way to go.

As always, financial planning and portfolio management should not be looked at in a vacuum. While the data certainly suggests that lump sum investing often has the edge, your personal circumstances and risk tolerance are paramount.

If you’re uncertain which approach is right for you, consulting with a financial advisor at HFG Trust can provide clarity and confidence in your-decision making process. Contact us today!

Tyler Pearson, Wealth Planner