The world has no shortage of how-to investment books and articles. So why would I attempt to add to the pile of information? I entered the wealth management business in 1983, fresh out of college. It took more than a few years to hone my skills and learn what works and what doesn’t. Unfortunately, the opportunity for facts and truth are hard to come by even with the internet. What I’m sharing with the reader is 90% evidence and 10% my opinion. I will attempt to be transparent when I’m voicing my opinion as compared to the evidence.

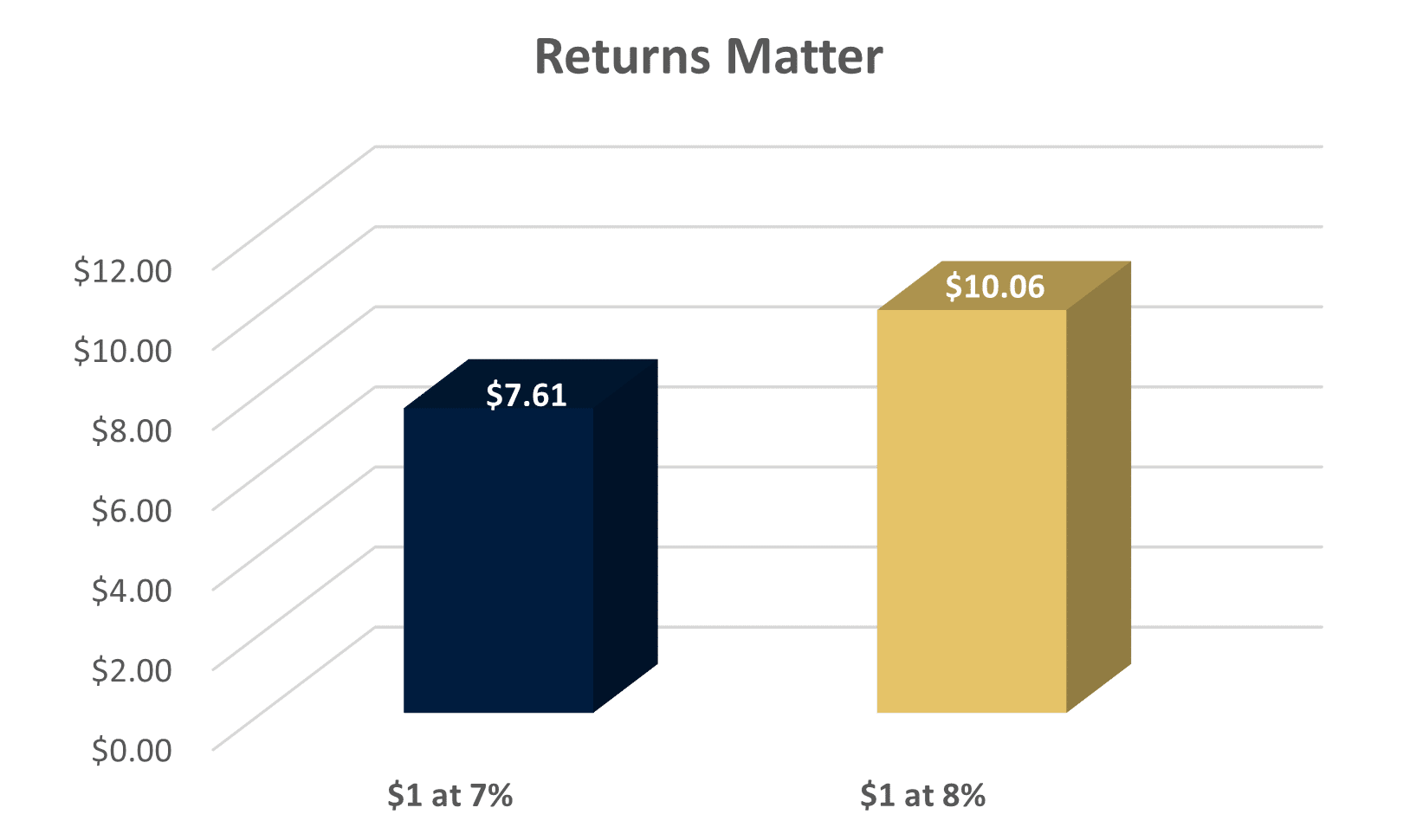

Number 1: Returns Matter

The power of compounding is remarkable. To illustrate, $1 invested over 30 years at 7% grows 7-fold, while an 8% return grows 10-fold. Thus, the additional 1% return creates a 40% higher ending value. Think about that. How would you feel about your financial security if your portfolio was 40% larger today?

We’ll go into a bit more detail on how these returns are generated in the following sections, but a key feature is portfolio allocation. Your investment portfolio should shift from primarily stocks when you are young, to an increasing allocation of bonds the closer you get to retirement. Being too conservative when you are young (owning too many bonds) can hurt your returns and be just as detrimental as having too much of your portfolio in stocks when you retire.

Number 2: Ownership is the Key to Long-Term Wealth

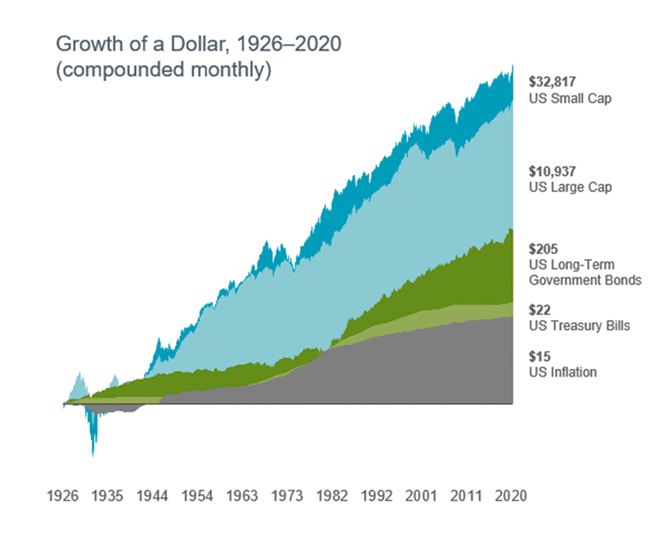

To keep investing simple, I encourage investors to see that investments are divided into two categories. You are either a lender or an owner. Lending types of investments are saving accounts, CDs, bonds, and mortgages. Since 1930, the average return of owning U.S. Treasury bonds has been around 4%. Ownership assets can be stocks, owning a small business, and real estate. Since 1930, the average return of US common stocks as measured by S&P 500 index has created a return of 10%.

Going back to our example of compounding $1 dollar over 30 years and comparing the growth at 4% vs. 10% is striking. At 4% the ending value is $3.20, while the same dollar at 10% is $17.40. If an investor had placed only 20% of their wealth in stocks at a 10% return and then spent the remaining 80% of wealth, they would have the same amount of wealth as the investor who invested the entire $1 at 4%. The takeaway is simple, if you have more than 20 years to retirement, you should be investing most of your wealth in ownership rather than trying to keep your money safe.

Number 3: Don’t Pick Stocks, Own the Market

This third point is crucial, and too few investors are aware of this long-known fact. There are two distinct investment philosophies. One group of investors attempts to distinguish stocks by having managers select a portfolio. The manager will interview the company, review their financials, or attempt to perform macro-economic analyses. This approach is called Active Management. The other method is called Indexing or Passive Management. Indexing is owning the entire market. Imagine hearing these two different conversations from two different investment advisors. Which of them sounds like a better approach?

-

- “Our firm works with Acme Global Strategic Advisors. They have offices all over the world and hire some of the brightest minds in the business. They meet with company leaders and review their financials before building a diversified portfolio. Their approach is to be active and responsive to economic conditions.”

- “Our firm builds a global portfolio of stocks by buying the market, which means we own almost every publicly traded company in the index. We don’t try to predict the market’s short-term moves and encourage our client’s to be patient during market declines.”

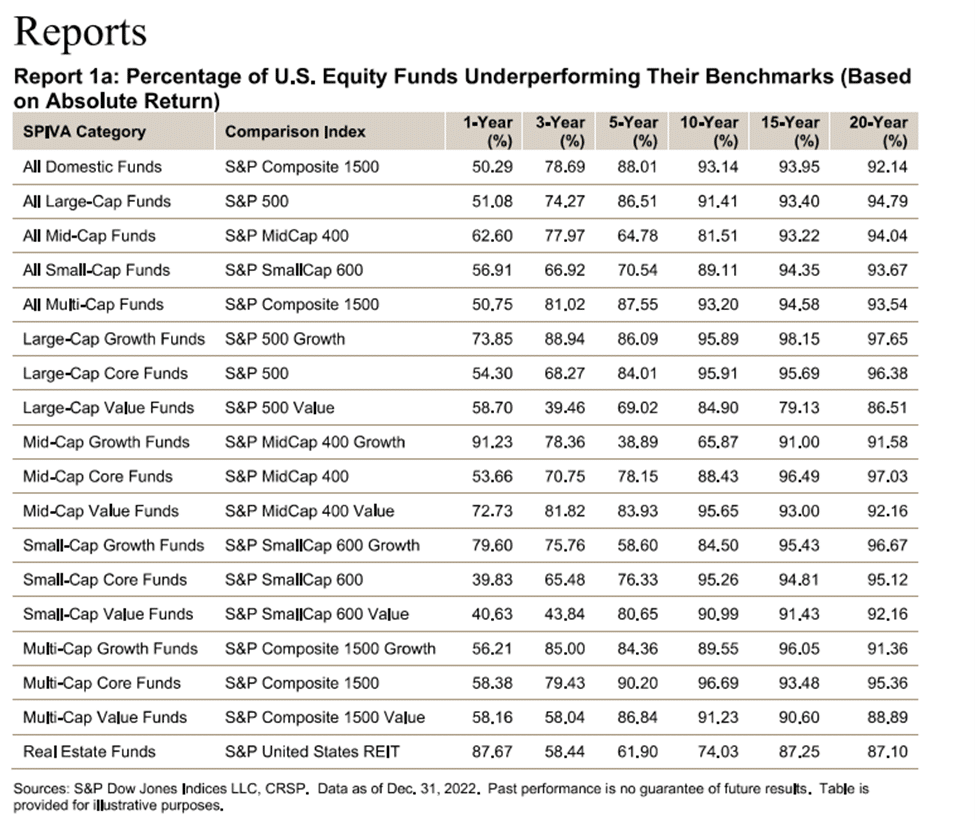

As you ponder these two approaches, let’s ask the question that needs to be answered. What have been the historical odds of all active managers beating the market vs a broadly diversified index? If you would like to research the answer, I encourage you to search for the “SPIVA Report” on Google. SPIVA stands for Standard & Poor Index vs. Active report. Twice a year, the SPIVA report is produced comparing the collective returns of Active managers to broadly diversified indices. When examining the results over 10- and 20-year time periods, Active Management has an average failure rate of 80-90%. Yes, you read it correctly. Active management underperforms indexing 80-90% of the time over long-time horizons. Why would any calculating investor use Active Management as their foundational strategy with such a low success rate? The answer – they weren’t presented with the facts. In the most recent SPIVA report, the underperformance cost investors over 1% in return per year. Do you know your advisor’s investment strategy?

Number 4: Consider Factor Investing

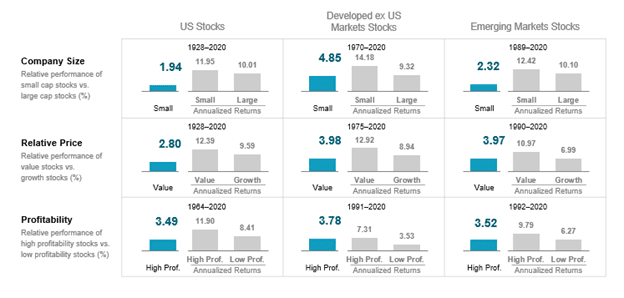

I am a strong proponent of using an index or passive approach to your portfolio strategy. However, if you are open to historical methods that have demonstrated strategies to improve the returns of indexing, you need to be aware of the research of Eugene Fama and Kenneth French, which built on Fama’s Nobel Prize winning work on the analysis of asset prices and the efficient market hypothesis. I am going to discuss two of the most significant findings of their research.

First, they determined that small stocks had provided higher returns as compared to large stocks. Their research started in 1928 and through 2022, small stocks have had an approximate 2% return advantage over large stocks. A US based index of the Russell 3000 or S&P 1500 would weigh small stocks at approximately 10% of the index. This means, if you invested $100,000 in either of these indexes, approximately $10,000 would be in small stocks. If we changed the composition of a portfolio to 20-30% in small stocks, we are tilting the portfolio to potentially higher returns. Thus, the improved portfolio would have an allocation with more small stocks compared to either of the indices.

The second factor is called Relative Price. Fama and French performed a financial calculation on every stock called the Price to Book ratio. This is where a stock’s market price is divided by the company’s Book Value. Book Value is the accounting value of the company. Stocks with higher Price to Book (PTB) ratios were called Growth stocks, while stocks with lower PTB ratios were called Value stocks. Their research found that since 1928, value stocks had an approximate 3% yearly return advantage over growth stocks. To improve upon indexing, if an investor overweighted the portfolio to value stocks, and if history repeats itself, investors could generate higher returns than the index.

The method of improving returns with Factor Investing is complicated for the average investor that isn’t educated in finance and accounting. However, there is historical evidence that using Factor Investing could enhance returns.

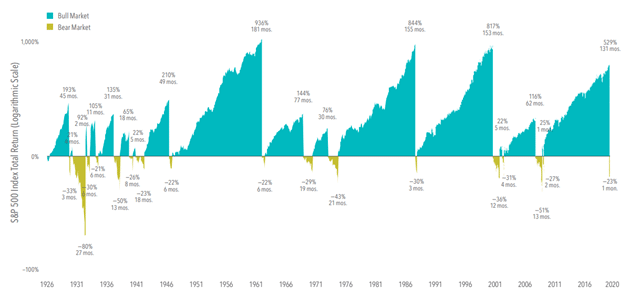

Number 5: Stay In Your Seat

The last strategy to improve returns is what I call “Staying in Your Seat”. Think of investing as watching a movie. If you leave your seat before the movie ends, you won’t see the ending. In my almost 40-years of practice, I see this affliction often with new clients.

After the market decline of 1987 (a single day decline of 19%), 2000-2002 (decline of 40%), 2008 (decline of 37%) and the first quarter of 2020 (decline of 20-30%), how many of you made changes to your 401(k) or portfolio? Did you add stocks during these market declines? Vanguard periodically issues its “Principles for Investing Success Report”. The report includes a section comparing the returns of different investment funds and what investors in the fund actually earned. Investor returns lagged behind the funds between -0.40 and -1.18% from December 2009 to December 2019.

Why such a difference? Most investors forgot that turbulence is a feature, not a bug in the market. Investors sold during market dips and repurchased after it had recovered. The summary is key, don’t SELL during market declines! Rather, turn off the financial news, stop monitoring your statements, and lead life as if the market didn’t exist. Warren Buffett has been quoted as saying that if the market closed for the next 10 years, it would have no impact on his investing.

At Community First Bank and HFG Trust, our team of experts are focused on helping you live the life you envision. If you have any questions or would like to review your plan, connect with an HFG Trust Advisor today.

Ty Haberling, CFP®

Founder, Board Member